What are Agentic Wallets? A 5-Minute Explainer

What are Agentic Wallets? A 5-Minute Explainer

Agentic wallets, explained: what they are, how they work, what's actually shipping, and what's still broken. A 5-minute primer.

May 11, 2026 — 7 min read

Agentic wallets are suddenly everywhere.

Coinbase launched ‘Agentic Wallets’ to give any agent a wallet. In the last week, Stripe and Binance launched their versions of agentic wallets.

At a more foundational level, Visa (Intelligent Commerce) and Mastercard (Agent Pay) are trying to define standards for how AI agents transact.

The pitch is consistent: give AI agents controlled yet autonomous access to money.

However, products, prototypes, and promises aren’t consistent. ‘Agentic wallets’ currently means very different things across teams.

So let's start from scratch. What an agentic wallet actually is, how it works, what are the use cases, tradeoffs, and everything in between.

What Are Agentic Wallets?

Agentic wallets are programmable wallets that can act on behalf of a user, within defined rules, without requiring constant human approval.

3 specific things make them different from a normal wallet:

Principal: An agentic wallet assumes the decision-maker is an AI agent acting on someone's behalf.

Policy: The rules are part of the wallet. Spending caps, allowlists, time bounds, revocation are all coded and enforced perennially.

Persistence: Agentic wallets are built to operate without any human watching. This means, humans can program transactions to happen 24/7.

Fact: Authentication ironically flips from using CAPTCHA to identify bots posing as humans to evaluating "is this agent allowed to do this, right now, for this human?”

Now, if we zoom out and rethink, ERC-4337 promised something similar in ‘smart wallets’.

What Every Smart Wallet Already Has

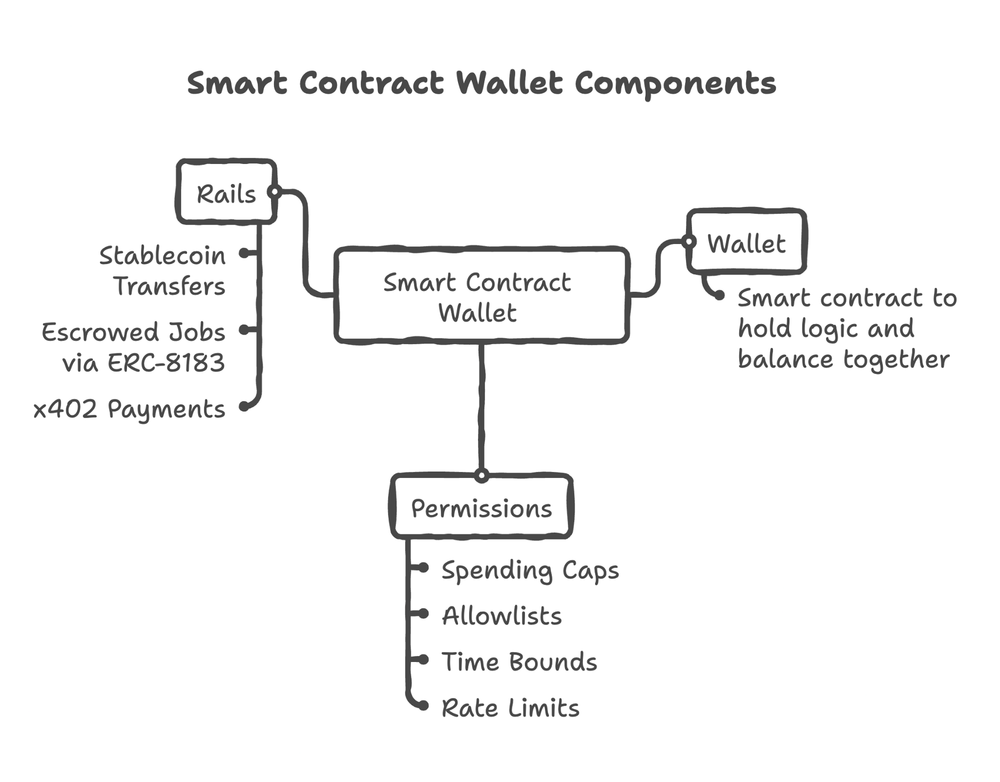

Most of what people call an ‘agentic wallet’ is built on top of a system that already exists: a programmable (smart) wallet.

Every smart wallet, agentic or not, has these three: wallet, permissions, and rails.

Smart wallets have these 3 parts already and aren’t agentic yet. Now, what brings the agentic capabilities to these wallets?

The Agentic Layer: What Makes a Wallet Agentic?

This is where the principal shifts. The wallet doesn’t ‘become intelligent’, it exposes controlled execution surfaces that an agent can use.

The cleanest way to think about the working of agentic wallets is:

Decision → Policy → Execution → Signing → Chain

Agentic wallets do not simply ‘think’ and move money.

Every action has to pass through constraints, compilation, authorization, and final settlement.

Decision: What Should Happen?

Agents observe inputs: user intent, balances, market data, API responses, onchain state, etc. It then expresses an intent, like:

pay for this API > swap X for Y > rebalance this position

At this stage, there is no transaction yet. Just a proposed action.

Policy: Should This Be Allowed?

Policy is where the wallet refuses to trust the model by default.

Wallets are embedded with offchain checks like:

spend limits

allowlists

rate limits

time bounds

merchant or contract restrictions

Some policies can also be enforced later at the account level, but the first gate is usually offchain because it is cheaper, faster, and easier to update.

Execution: How Does Intent Become a Transaction?

Execution turns intent into something the blockchain can accept.

This includes:

route selection

calldata construction

state assumptions

gas estimation

dry-run simulation

revert detection

This is where ‘rebalance portfolio’ becomes a concrete sequence of calls.

Signing: Who Authorizes the Transaction?

Signing is the enforcement power users give to agentic wallets and something that differentiates them from smart wallets.

This is where scoped authority becomes real through:

session keys

MPC / threshold keys

TEE-backed keys

smart account validation

The key point: the agent should not hold unlimited authority. It should hold constrained signing power.

Blockchain: Final Settlement

Transactions are submitted via relayers or bundlers and executed onchain. This is where:

state changes finalize

value moves

outcomes become irreversible

Agentic wallet builders, for this phase of the transaction, need to think through multiple scenarios like MEV, latency, failed execution, etc and ensure wallets have the ability to navigate without needing a human.

To sum up, agentic wallets automate decisions and transactions is a half-truth.

The reality is agentic wallets automate decision-making and execution only if policy, signing, and settlement keep the agent constrained.

The model is clear. The question is: where does this actually work today?

What Can We Actually Do With an Agentic Wallet Today?

Honestly, most ‘agentic wallets’ today are still human-in-the-loop checkouts like ChatGPT Instant Checkout, Microsoft Copilot, Stripe Link with agent delegation.

The agent recommends, builds the cart, drafts the transaction and needs a human to tap ‘confirm’.

The genuinely autonomous end of the spectrum is narrower, but real. Here are a few use cases that are live:

Pay-per-call APIs: An agent can authenticate, pay, and consume in a single HTTP round trip.

CoinGecko offers x402-enabled endpoints at $0.01 USDC per request.Autonomous DeFi: Agents can monitor markets, rebalance positions, and execute trades within constraints.

Supermission runs multi-step DeFi operations across 10 AI agents on 4 chains without an API key.

Mamo routes ~$58M in volume across Moonwell and Morpho on Base via per-user smart accounts.

Giza ARMA holds ~$40M+ AUM allocating stablecoins across Aave, Morpho, Moonwell, and Fluid.Prediction market agents: Agentic wallets scan markets in real-time, place trades on behalf of the user, and participate 24/7 in prediction markets.

Olas Polystrat produces 8.2M+ on-chain transactions and is the highest-volume autonomous agent deployment onchain today.

Outside these three, there are notable agent-to-agent commerce efforts like Daydreams which operates a closed loop where an agent buys its own LLM inference from another agent it knows.

The pattern is consistent: autonomy is working where the loop is tight, the cost of failure is bounded, and the environment is programmable.

But, are agentic wallets ready and complete?

Trust and Tradeoffs: Why Are Agentic Wallets Still Not Complete?

Agentic wallets, as an infrastructure, are nascent but growing quickly. It has the ability to unlock a plethora of use cases for AI.

However, not yet. Why? Here are a few critical reasons:

Prompt Injection Isn't Solved

An agent that reads webpages, emails, or product descriptions can be instructed by anything hidden in those documents.

Google researchers noted a 32% rise in malicious instructions embedded in HTML. This included specified payment payloads aimed at agents with payment authority.

Policy Is Still Primitive

Most systems today rely on a mix of static limits (spend caps, allowlists), offchain checks, and best-effort validation.

That works for simple flows. It breaks as soon as decisions require judgment.

But, policies or rules that are:

expressive enough to handle real-world context

strict enough to prevent misuse

flexible enough to evolve over time,

is still an open problem.

Enforcement Happens Too Late

Decisions are made offchain. Enforcement happens at signing or onchain.

Everything in between — intent formation, execution planning, simulation — is a soft and vulnerable layer.

By the time a transaction reaches onchain validation:

the decision is already made

the system is biased toward execution

Onchain checks can reject invalid transactions, but they cannot determine whether the decision itself was correct.

None of this is a reason to stop building. It's a reason to build with eyes open.

Agentic Wallets Aren’t Magic. The Hard Parts Are Still Unsolved

Most of the core pieces already exist: programmable accounts, delegated signing, intent frameworks, and emerging payment rails.

What’s missing is reliability.

> Policy is still ad hoc and offchain.

> Trust relies on simulation and heuristics.

> Decisions remain unbounded and hard to audit.

Solving these is an infrastructure and verification problem. Unless these are fixed, autonomy will stay narrow and constrained.

About Quicknode

Founded in 2017, Quicknode deploys institutional-grade blockchain infrastructure for developers and enterprises. With 99.99% uptime and support for 80+ chains, teams build and scale onchain applications without compromise.

Stay updated

The latest engineering insights, product updates, and web3 news delivered straight to your inbox.